UCSD Triton Quantitative Trading Club Lead, Strategy Development Research Group

March 2026 – present

- Constructing a suite of delta-hedged options strategies in QuantConnect, implementing vega-scaled positioning, IV percentile filtering, and automated Greeks-based entry and exit logic across long/short vega and gamma regimes on SPY.

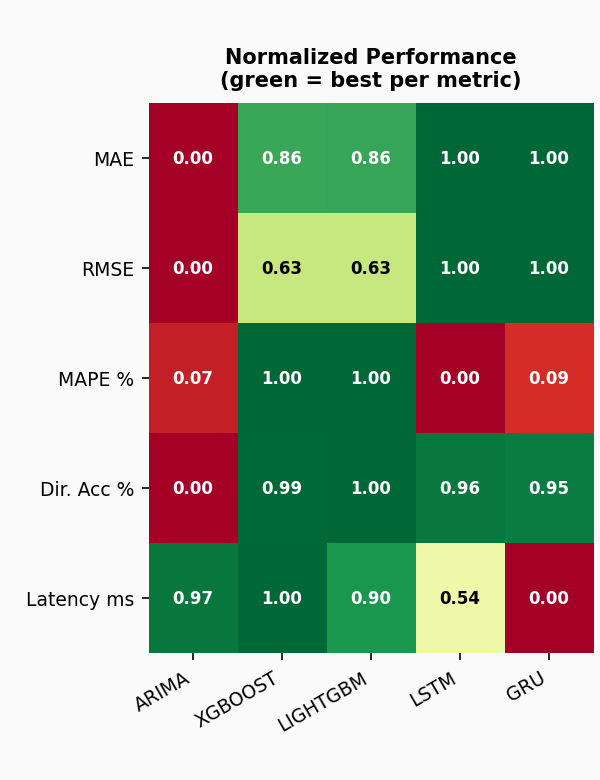

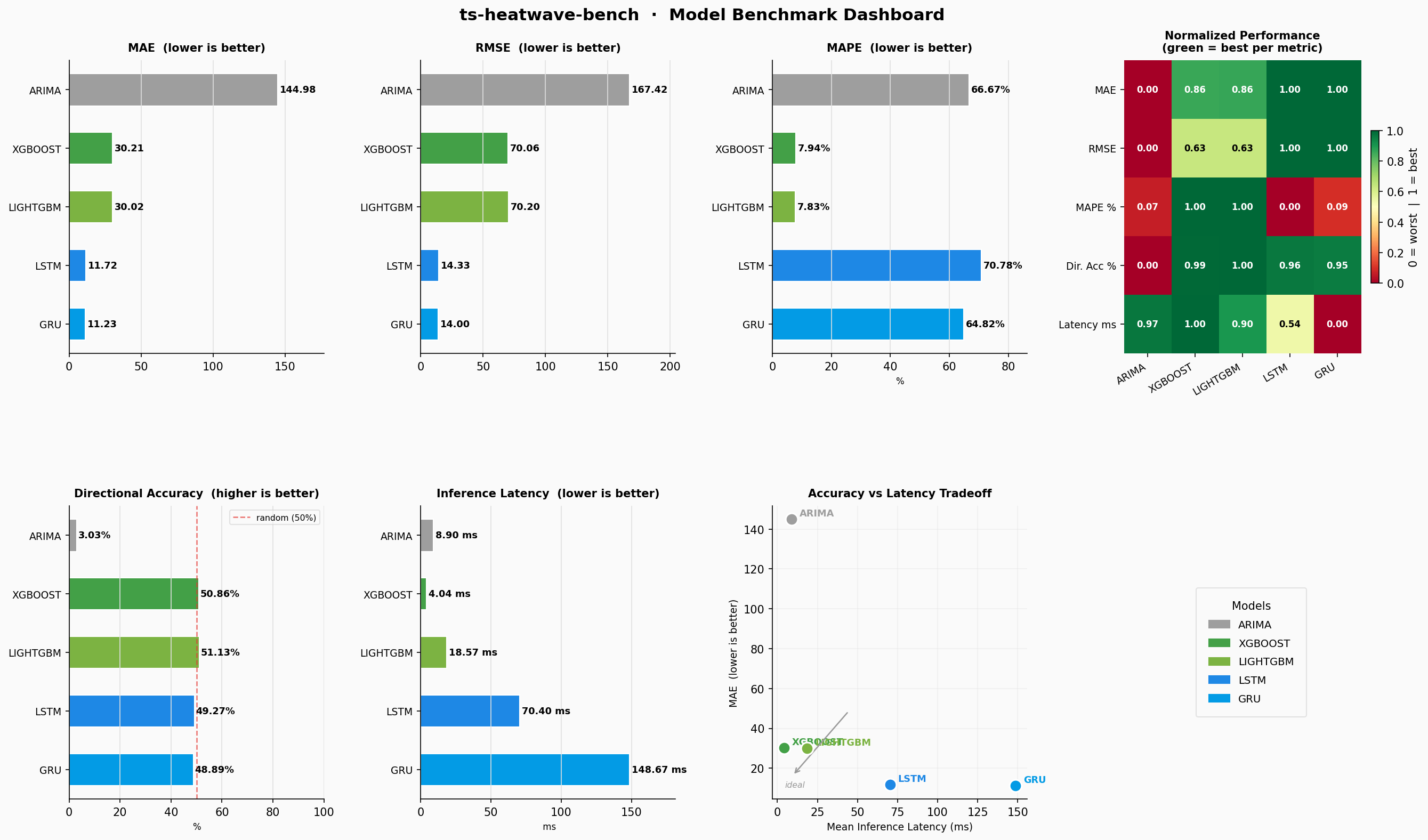

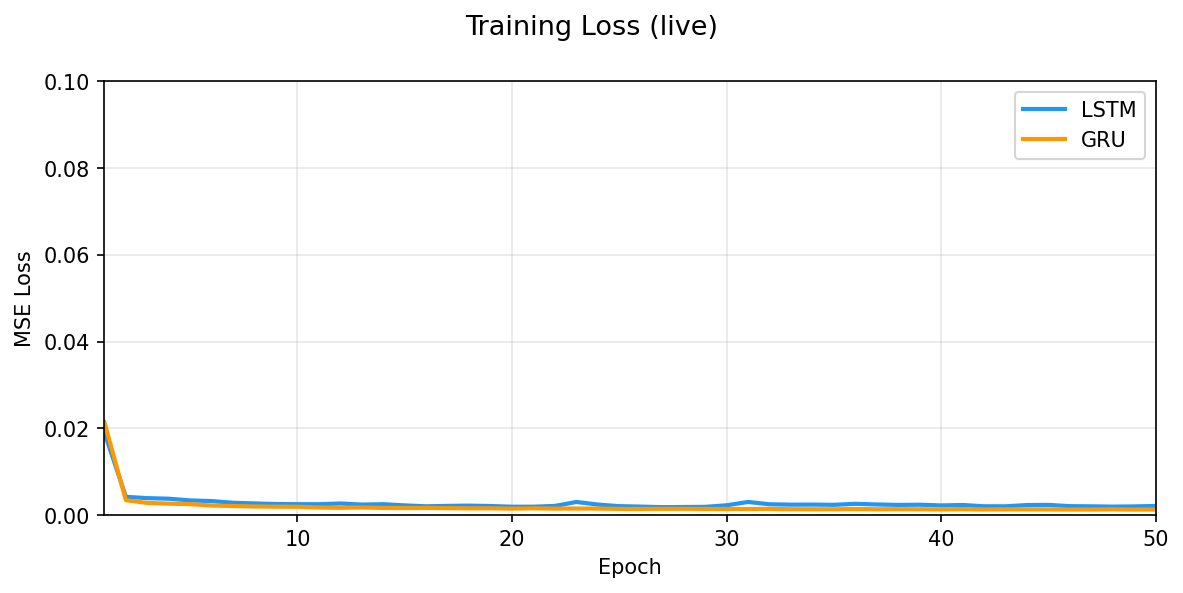

- Built a multi-architecture volatility forecasting benchmark comparing gradient boosting (XGBoost/LightGBM) against sequential deep learning models (LSTM, GRU, Temporal Transformer) on realized SPY volatility, with a shared evaluation harness and reproducible results.

- Constructed an in-database ML forecasting pipeline using MySQL HeatWave, benchmarking time series model performance against external Python baselines; documenting tradeoffs in latency, accuracy, and scalability.